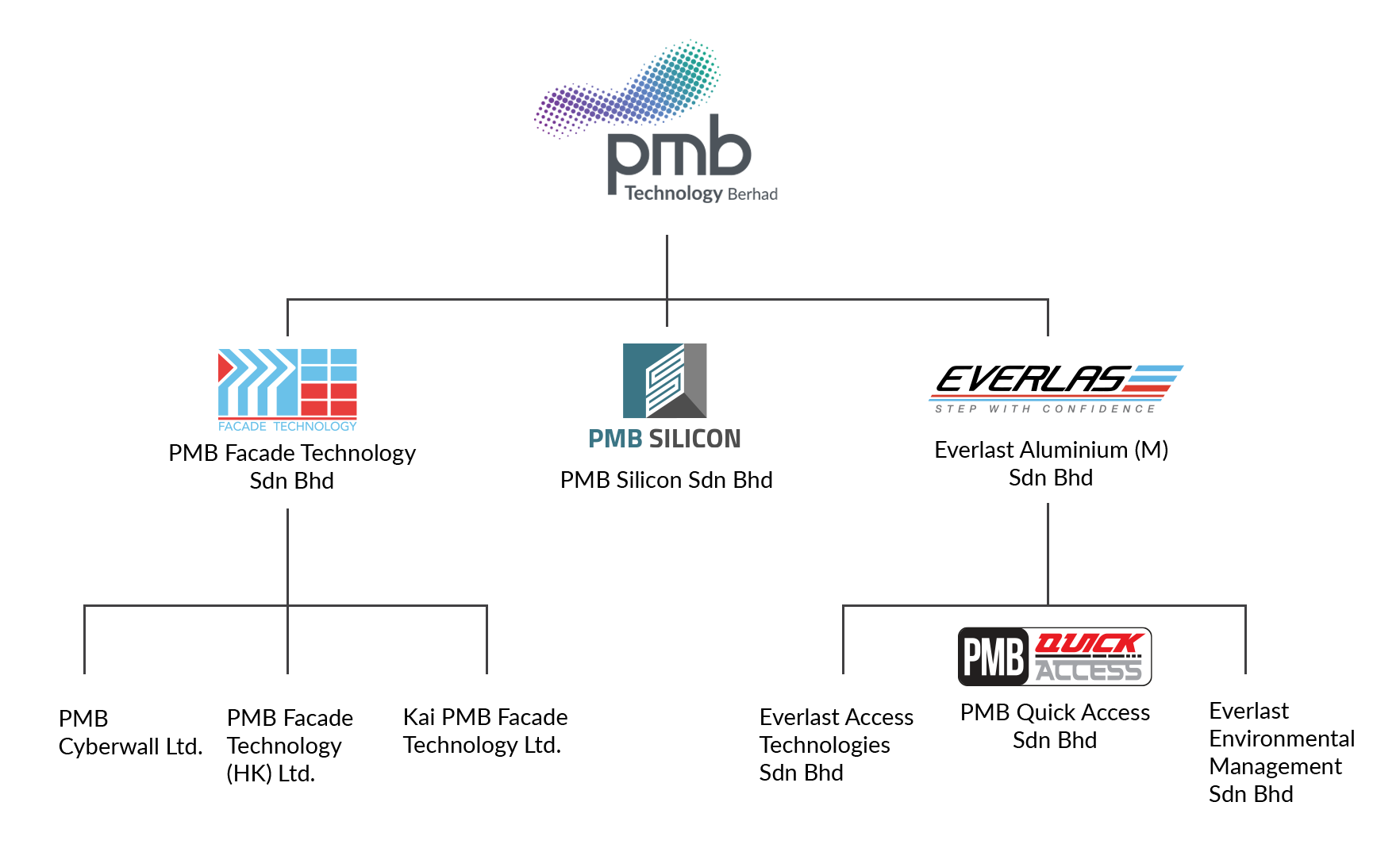

Silicon smelter

and producer

Design, fabrication and

installation of aluminium

curtain wall and

formwork system

Marketing and leasing

of boom lift machinery

and manufacturing of

aluminium mobile

Manufacturing and

marketing of aluminium

ladder and product

We take great pride in our unwavering dedication towards building a superior supply chain, enhancing customer satisfaction, minimizing emissions and waste, and addressing social inequalities. By aligning ourselves with UN-certified green practices, we demonstrate our commitment to the environment.

|

|